The Importance of Financial Planning Before Taking a Loan in Corinth, MS

February 12, 2025

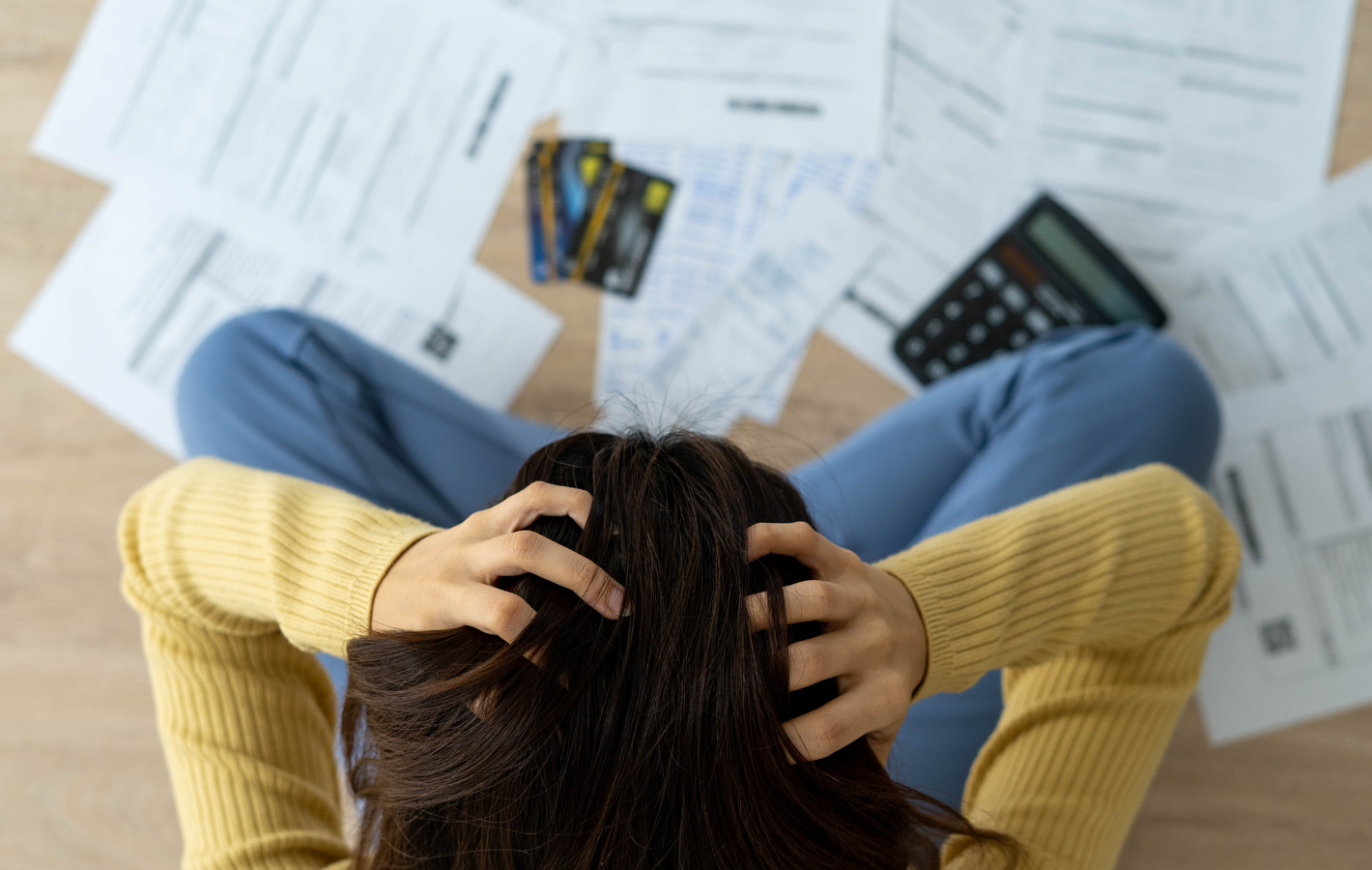

Taking out a loan is a significant financial decision that requires careful planning and consideration. Whether you're looking for a personal loan, a cash loan, or a payday loan, having a solid financial plan in place can help ensure that you make the best choices for your financial health. For residents of Corinth, Mississippi, Family Financial Services offers a range of loan options, but before you proceed, it's crucial to understand the importance of financial planning. In this blog, we will explore why financial planning is essential before taking a loan and provide actionable steps to help you prepare.

Why Financial Planning is Essential

Avoiding Over-Borrowing

One of the primary reasons financial planning is essential before taking out a loan is to avoid over-borrowing. Without a clear understanding of your financial situation, it's easy to borrow more money than you need or can comfortably repay. Over-borrowing can lead to higher monthly payments, increased interest costs, and financial strain.

Ensuring Loan Affordability

Financial planning helps you determine whether you can afford the loan repayments without compromising other essential expenses. By evaluating your income, expenses, and financial obligations, you can ensure that you choose a loan amount and repayment term that fit within your budget.

Minimizing Financial Stress

Taking out a loan without proper planning can lead to financial stress and anxiety. By having a clear plan in place, you can manage your loan repayments with confidence, knowing that you have accounted for all potential challenges and have a strategy to address them.

Achieving Financial Goals

A well-thought-out financial plan allows you to align your loan with your broader financial goals. Whether you're looking to consolidate debt, finance a major purchase, or cover emergency expenses, planning ensures that your loan supports your overall financial objectives.

Steps for Effective Financial Planning

1. Assess Your Financial Situation

Evaluate Income and Expenses

Start by evaluating your current financial situation. Calculate your monthly income from all sources and list your monthly expenses, including rent/mortgage, utilities, groceries, transportation, and any other regular payments. This assessment will give you a clear picture of your cash flow and help you determine how much you can allocate towards loan repayments.

Identify Financial Obligations

Take stock of your existing financial obligations, such as credit card balances, other loans, and any outstanding debts. Understanding your total debt load is crucial for determining your capacity to take on additional debt.

2. Set Clear Financial Goals

Short-Term and Long-Term Goals

Define your short-term and long-term financial goals. Are you looking to pay off high-interest debt, fund a home renovation, or cover unexpected medical expenses? Having clear goals will guide your borrowing decisions and ensure that your loan aligns with your financial objectives.

Prioritize Goals

Prioritize your financial goals based on urgency and importance. This prioritization will help you decide which goals to address first and how to allocate your resources effectively.

3. Determine Loan Amount and Repayment Term

Calculate Loan Amount

Based on your financial assessment and goals, calculate the loan amount you need. Avoid borrowing more than necessary, as this will increase your repayment burden and interest costs. Be realistic about the amount you need and can comfortably repay.

Choose Repayment Term

Consider the repayment term that best fits your financial situation. A shorter repayment term will result in higher monthly payments but lower total interest costs, while a longer term will have lower monthly payments but higher total interest costs. Choose a term that balances affordability with minimizing interest.

4. Compare Loan Options

Research Lenders

Research different lenders to find the best loan options available. Family Financial Services in Corinth, MS, offers competitive rates and personalized service, but it's also wise to compare their offerings with other local and online lenders to ensure you're getting the best deal.

Evaluate Loan Terms

Compare the interest rates, fees, and repayment terms of various loan options. Pay attention to the annual percentage rate (APR), which includes both the interest rate and any fees, providing a comprehensive view of the loan's cost.

5. Plan for Repayment

Create a Repayment Plan

Develop a detailed repayment plan that outlines how you will make your loan payments. Include the loan amount, interest rate, repayment term, and monthly payment amount. Ensure that your plan fits within your budget and allows you to meet other financial obligations.

Build an Emergency Fund

Having an emergency fund can provide a financial cushion in case of unexpected expenses or changes in your financial situation. Aim to save enough to cover 3-6 months of living expenses to protect yourself against unforeseen challenges.

6. Monitor and Adjust Your Plan

Track Your Progress

Regularly monitor your progress towards repaying your loan and achieving your financial goals. Keep track of your payments, expenses, and any changes in your financial situation.

Adjust as Needed

Be prepared to adjust your financial plan as needed. If you experience changes in income, expenses, or financial goals, update your plan to reflect these changes. Flexibility is key to maintaining financial stability and ensuring successful loan repayment.

Conclusion

Financial planning is a critical step before taking out a loan in Corinth, Mississippi. By assessing your financial situation, setting clear goals, determining the right loan amount and repayment term, comparing loan options, and creating a repayment plan, you can ensure that your loan supports your financial health and goals. Family Financial Services is here to provide the support and guidance you need throughout the loan process, helping you make informed decisions and achieve your financial objectives with confidence. By taking the time to plan, you can manage your loan repayments effectively and enjoy the benefits of financial stability and success.

Applying for a loan can be a significant step toward achieving your financial goals, whether you’re looking to finance a major purchase, consolidate debt, or cover unexpected expenses. Understanding the loan approval process can help you navigate it with confidence and increase your chances of a successful application. For residents of Corinth, Mississippi, Family Financial Services offers a straightforward and supportive approach to loan approval. In this blog, we’ll walk you through what to expect during the loan approval process, from application to disbursement. 1. Initial Inquiry and Application Research and Pre-Qualification Before you formally apply for a loan, it’s a good idea to research your options and determine what type of loan best suits your needs. Family Financial Services offers various loan products, including personal loans, cash loans, same-day loans, and payday loans. Pre-qualification is often available and can give you an estimate of the loan amount and terms you might qualify for based on a preliminary review of your financial information. Application Submission The first step in the loan approval process is submitting your application. This can typically be done online or in-person at Family Financial Services. The application will require you to provide basic information, such as: Personal identification (e.g., driver’s license, passport) Proof of income (e.g., pay stubs, tax returns, bank statements) Employment details Information about your financial situation, including existing debts and monthly expenses 2. Documentation Review and Verification Gathering Required Documents After submitting your application, you will need to provide supporting documentation to verify the information you’ve provided. This may include: Income Verification: Recent pay stubs, tax returns, or bank statements to confirm your income. Identification: A valid government-issued ID to verify your identity. Employment Verification: Details about your current employment, such as an employer’s contact information or a letter of employment. Credit Report: Family Financial Services may request a copy of your credit report to assess your creditworthiness. Verification Process Family Financial Services will review and verify your documentation to ensure the accuracy and completeness of your application. This step is crucial for confirming your ability to repay the loan and assessing the risk involved. During this process, you might be contacted for additional information or clarification on certain points. 3. Credit Evaluation and Underwriting Credit Score Assessment Your credit score plays a significant role in the loan approval process. It helps the lender assess your creditworthiness and determine the interest rate and terms of your loan. A higher credit score typically results in better loan terms and lower interest rates. Family Financial Services will review your credit score and history as part of the evaluation. Underwriting Process Underwriting is the process where the lender evaluates your application, documentation, and credit information to make a final decision on your loan. The underwriter will consider factors such as your debt-to-income ratio, credit history, and the stability of your income. This process ensures that you meet the lender’s criteria for loan approval and helps determine the loan amount and terms you qualify for. 4. Loan Approval and Offer Approval Decision Once the underwriting process is complete, Family Financial Services will make a decision on your loan application. If approved, you will receive a loan offer that includes details such as the loan amount, interest rate, repayment term, and any associated fees. Reviewing the Offer It’s important to carefully review the loan offer to ensure you understand all the terms and conditions. Pay attention to the interest rate, monthly payment amount, repayment schedule, and any fees or penalties for early repayment. If you have any questions or concerns, don’t hesitate to contact Family Financial Services for clarification. Accepting the Loan If you’re satisfied with the loan offer, you will need to accept the terms and sign the loan agreement. This can typically be done electronically or in-person. Once you’ve accepted the loan, Family Financial Services will move forward with the disbursement process. 5. Loan Disbursement Receiving the Funds After you’ve signed the loan agreement, Family Financial Services will disburse the loan funds to your designated bank account. The time it takes to receive the funds can vary, but it’s often completed within a few business days. Same-day and payday loans may offer even faster disbursement times, depending on the specifics of the loan. Managing Your Loan Once you’ve received the loan funds, it’s important to manage your loan responsibly. Make sure to budget for your monthly payments and keep track of your repayment schedule. Setting up automatic payments can help ensure you never miss a payment and can also help you avoid late fees and penalties. 6. Post-Approval Support Ongoing Communication Family Financial Services is committed to providing ongoing support throughout the life of your loan. If you have any questions or encounter any issues with your loan repayments, don’t hesitate to reach out for assistance. Open communication can help you address any potential problems early and maintain a positive relationship with your lender. Financial Planning and Advice In addition to loan servicing, Family Financial Services can offer financial planning and advice to help you manage your finances more effectively. Whether you need assistance with budgeting, debt management, or saving strategies, their team is available to provide guidance and support. Conclusion Understanding the loan approval process can help you navigate it with confidence and ensure a smooth experience. From initial inquiry and application to documentation review, credit evaluation, and loan disbursement, each step is designed to assess your financial situation and determine the best loan options for your needs. Family Financial Services in Corinth, Mississippi, is dedicated to making this process as straightforward and supportive as possible. By choosing a trusted local lender, you can achieve your financial goals with confidence and ease. Contact Family Financial Services today to learn more about their loan products and how they can help you secure the funding you need.

Choosing the right loan can significantly impact your financial health and help you achieve your goals more effectively. With various loan options available, it's essential to understand your needs and evaluate the terms and conditions before making a decision. Family Financial Services in Corinth, Mississippi, offers a wide range of loan products designed to meet diverse financial needs. This blog will guide you through the process of selecting the right loan for your specific situation. Understanding Your Financial Needs Assess Your Situation Before you start comparing loan options, it’s crucial to assess your financial situation and determine your needs. Ask yourself the following questions: What is the purpose of the loan? (e.g., debt consolidation, home improvement, medical expenses) How much money do you need to borrow? What is your current financial status? (e.g., income, expenses, existing debts) How quickly do you need the funds? Define Your Goals Having clear financial goals will help you choose the right loan type. For instance, if you need to consolidate high-interest debt, a personal loan with a lower interest rate might be ideal. If you’re facing an emergency expense, a same-day or payday loan could provide quick access to funds. Types of Loans Available Personal Loans Overview Personal loans are versatile, unsecured loans that can be used for a variety of purposes. They typically come with fixed interest rates and repayment terms. Best For Debt consolidation Home improvements Medical expenses Major purchases Pros and Cons Pros: Fixed interest rates, predictable payments, no collateral required Cons: Requires good credit for favorable rates, potential origination fees Cash Loans Overview Cash loans, or payday loans, are short-term loans designed to provide immediate financial relief until your next paycheck. Best For Emergency expenses Short-term financial needs Pros and Cons Pros: Fast approval and funding, minimal credit requirements Cons: High interest rates, short repayment terms Same-Day Loans Overview Same-day loans offer quick access to funds, typically within hours of application, making them ideal for urgent financial needs. Best For Immediate financial emergencies Unexpected expenses Pros and Cons Pros: Rapid access to funds, simple application process Cons: Higher interest rates, short repayment periods Payday Loans Overview Payday loans are small, short-term loans intended to cover expenses until your next payday. They are known for their quick approval and funding process. Best For Temporary financial shortfalls Urgent bills or expenses Pros and Cons Pros: Easy qualification, fast funding Cons: High interest rates, must be repaid quickly Auto Loans Overview Auto loans are secured loans specifically for purchasing a vehicle, using the vehicle as collateral. They typically offer lower interest rates compared to unsecured loans. Best For Purchasing a new or used vehicle Pros and Cons Pros: Lower interest rates, flexible terms Cons: Requires collateral, potential for repossession if defaulted Business Loans Overview Business loans provide financing for various business needs, from expanding operations to purchasing equipment. Best For Business expansion Equipment purchases Managing cash flow Pros and Cons Pros: Supports business growth, flexible use of funds Cons: May require collateral, detailed documentation needed Factors to Consider When Choosing a Loan Interest Rates The interest rate is a crucial factor in determining the overall cost of the loan. Compare rates from different lenders to find the most competitive option. Remember that lower interest rates can save you a significant amount of money over the life of the loan. Repayment Terms Consider the loan’s repayment term and how it fits into your budget. Shorter terms typically have higher monthly payments but lower total interest costs. Longer terms have lower monthly payments but can be more expensive overall due to interest. Fees and Charges Be aware of any fees associated with the loan, such as origination fees, prepayment penalties, or late payment charges. These additional costs can affect the affordability of the loan. Loan Amount Ensure the loan amount meets your needs without encouraging over-borrowing. Borrowing more than necessary can lead to higher repayments and increased financial strain. Lender Reputation Choose a reputable lender with positive customer reviews and a track record of transparent and fair practices. Family Financial Services in Corinth, MS, is known for its customer-focused approach and reliable loan products. Steps to Apply for a Loan Gather Necessary Documentation Prepare the required documents for your loan application, which may include proof of income, identification, and financial statements. Having these documents ready can expedite the application process. Compare Loan Options Research and compare different loan options from various lenders. Use online comparison tools and read customer reviews to ensure you choose the best loan for your needs. Submit Your Application Complete the loan application with accurate and complete information. Family Financial Services offers both online and in-person application options for your convenience. Review Loan Terms Once you receive a loan offer, carefully review the terms and conditions. Ensure you understand the interest rate, repayment schedule, fees, and any other important details before accepting the loan. Accept the Loan If you’re satisfied with the loan terms, sign the agreement and proceed with the loan acceptance process. Family Financial Services will disburse the funds to your bank account promptly. Conclusion Choosing the right loan for your needs in Corinth, Mississippi, involves careful consideration of your financial situation, goals, and the available loan options. By understanding the different types of loans and evaluating factors such as interest rates, repayment terms, and fees, you can make an informed decision that supports your financial well-being. Family Financial Services is dedicated to providing a range of loan products and personalized support to help you achieve your financial objectives. Contact them today to learn more about how they can assist you in finding the perfect loan for your needs.

Securing a loan can be a crucial step towards achieving your financial goals, whether it's for personal expenses, consolidating debt, or making a major purchase. For residents of Corinth, Mississippi, understanding the different types of loans available can help you make an informed decision and choose the best option for your needs. Family Financial Services offers a variety of loan products tailored to meet the diverse financial needs of the community. In this blog, we will explore the different types of loans available in Corinth, MS, and highlight their key features and benefits. 1. Personal Loans Overview Personal loans are versatile, unsecured loans that can be used for a wide range of purposes, such as home improvements, medical expenses, travel, or consolidating high-interest debt. Because they are unsecured, personal loans do not require collateral, but approval and interest rates depend on your credit score and financial history. Benefits Flexible Use: Funds can be used for virtually any purpose. Fixed Interest Rates: Predictable monthly payments with fixed interest rates. No Collateral Required: Approval based on creditworthiness rather than assets. How to Apply Applying for a personal loan with Family Financial Services is straightforward. You'll need to provide proof of income, identification, and other financial information. The application can be completed online or in-person for your convenience. 2. Cash Loans Overview Cash loans, also known as payday loans, are short-term loans designed to provide quick access to funds for immediate needs. These loans are typically repaid on your next payday and are ideal for covering unexpected expenses or emergencies. Benefits Fast Access to Funds: Quick approval and funding, often within the same day. Minimal Requirements: Fewer documentation requirements compared to other loans. No Credit Check: Suitable for borrowers with poor or no credit history. How to Apply To apply for a cash loan, you will need proof of income, identification, and your bank account details. Family Financial Services offers a streamlined application process to get you the funds you need quickly. 3. Same-Day Loans Overview Same-day loans are designed for borrowers who need immediate financial assistance. These loans offer fast approval and disbursement, ensuring you can address urgent financial needs without delay. Benefits Immediate Funding: Access to funds within hours of application. Convenient Process: Simple application process with quick decision-making. Emergency Use: Ideal for medical emergencies, urgent repairs, or other unexpected expenses. How to Apply Applying for a same-day loan with Family Financial Services involves providing basic information such as proof of income and identification. The process is designed to be quick and hassle-free. 4. Payday Loans Overview Payday loans are short-term, high-interest loans intended to cover immediate financial needs until your next payday. These loans are typically smaller amounts and are repaid in full on your next payday. Benefits Quick Approval: Fast processing and funding, often within the same day. Easy Qualification: Minimal credit requirements, making it accessible for those with low credit scores. Short-Term Solution: Provides a quick fix for temporary financial shortfalls. How to Apply To apply for a payday loan, you will need to provide proof of income, identification, and your bank account details. Family Financial Services offers a straightforward application process to get you the funds you need promptly. 5. Auto Loans Overview Auto loans are secured loans specifically designed for purchasing a vehicle. The vehicle itself serves as collateral, which can result in lower interest rates compared to unsecured loans. Auto loans typically offer flexible repayment terms and fixed interest rates. Benefits Lower Interest Rates: Often lower than unsecured loans due to collateral. Flexible Terms: Choose repayment terms that fit your budget. Fixed Monthly Payments: Predictable payments with fixed interest rates. How to Apply Applying for an auto loan with Family Financial Services involves providing information about the vehicle you intend to purchase, proof of income, and identification. The approval process is quick, allowing you to secure financing and purchase your vehicle without delay. 6. Business Loans Overview Business loans provide financing for various business needs, such as expanding operations, purchasing equipment, or managing cash flow. These loans can be secured or unsecured, depending on the amount and purpose of the loan. Benefits Support for Business Growth: Funds to expand operations, purchase inventory, or invest in new opportunities. Flexible Terms: Various repayment options to suit your business needs. Tailored Solutions: Customized loan products to meet specific business requirements. How to Apply To apply for a business loan, you will need to provide your business plan, financial statements, and other relevant documentation. Family Financial Services offers personalized support to help you navigate the application process and secure the financing your business needs. Tips for Choosing the Right Loan Assess Your Financial Needs Determine the specific purpose of the loan and the amount you need to borrow. This will help you choose the most appropriate loan type and avoid over-borrowing. Check Your Credit Score Your credit score can impact your loan eligibility and interest rates. Check your credit score before applying and take steps to improve it if necessary. Compare Loan Options Research and compare different loan options and lenders to find the best terms and interest rates. Consider factors such as repayment terms, fees, and overall cost. Understand Loan Terms Read the terms and conditions of the loan carefully. Make sure you understand the interest rate, repayment schedule, fees, and any penalties for late payments or early repayment. Conclusion Understanding the different types of loans available in Corinth, Mississippi, can help you make informed decisions and choose the best option for your financial needs. Family Financial Services offers a variety of loan products, including personal loans, cash loans, same-day loans, payday loans, auto loans, and business loans. With their competitive rates, personalized service, and commitment to the local community, Family Financial Services is here to support you in achieving your financial goals. Whether you need funds for personal expenses, a new vehicle, or business expansion, they provide the financial solutions you need with the simplicity and care you deserve. Contact Family Financial Services today to learn more about their loan products and how they can help you achieve your financial objectives.

Securing a loan can often seem like a complex and daunting task. However, Family Financial Services in Corinth, Mississippi, is dedicated to making the loan process straightforward and stress-free for its clients. Whether you need a personal loan, a cash loan, or a payday loan, Family Financial Services offers a streamlined approach to help you get the funds you need quickly and efficiently. In this blog, we’ll explore how Family Financial Services simplifies the loan process and why they are the best choice for your financial needs in Corinth, MS. 1. User-Friendly Application Process Online and In-Person Applications Family Financial Services understands that convenience is key when it comes to applying for a loan. They offer both online and in-person application options to accommodate your preferences and schedule. The online application process is designed to be quick and easy, allowing you to apply from the comfort of your home or office. If you prefer a more personal touch, you can visit their office in Corinth, MS, where friendly staff are ready to assist you. Minimal Documentation Required To make the application process as smooth as possible, Family Financial Services requires minimal documentation. Typically, you will need to provide: Proof of identity (such as a driver’s license or passport) Proof of income (such as recent pay stubs or bank statements) Bank account details for fund disbursement This streamlined documentation requirement helps expedite the approval process, getting you the funds you need without unnecessary delays. 2. Fast Approval and Funding Quick Decision-Making One of the standout features of Family Financial Services is their commitment to quick decision-making. They understand that when you need a loan, time is often of the essence. The loan approval process is designed to be fast, with most decisions made within hours of receiving your application. This rapid turnaround time means you won’t be left waiting and wondering about the status of your loan. Immediate Fund Disbursement Once your loan is approved, Family Financial Services ensures that the funds are disbursed to your bank account as quickly as possible. This immediate access to funds is crucial for managing emergencies, unexpected expenses, or time-sensitive financial needs. Whether you’re dealing with a medical bill, car repair, or any other urgent expense, you can count on Family Financial Services to provide prompt financial support. 3. Competitive Interest Rates and Transparent Terms Affordable Financing Family Financial Services offers competitive interest rates on all their loan products. By providing affordable financing options, they help you manage your loan repayments without straining your budget. Lower interest rates mean lower monthly payments, making it easier to stay on track with your financial goals. Clear and Transparent Terms Understanding your loan terms is essential for effective financial planning. Family Financial Services prides itself on offering clear and transparent loan terms. There are no hidden fees or unexpected charges; everything is laid out plainly so you know exactly what to expect. This transparency builds trust and ensures that you can make informed decisions about your financial future. 4. Personalized Customer Service Individualized Attention At Family Financial Services, personalized customer service is at the heart of their operations. Their team takes the time to understand your unique financial situation and tailor their loan offerings to meet your specific needs. Whether you need help choosing the right loan product or have questions about the application process, their knowledgeable staff is there to provide individualized attention and support. Ongoing Support Family Financial Services doesn’t just stop at providing loans; they are committed to supporting you throughout the life of your loan. If you encounter any issues or have questions about your loan, their team is always available to assist. This ongoing support ensures that you feel confident and secure in your financial decisions. 5. Local Expertise and Community Commitment Understanding Local Needs As a local lender in Corinth, MS, Family Financial Services has a deep understanding of the community’s unique financial needs. This local expertise allows them to offer loan products and services that are specifically tailored to the residents of Corinth and the surrounding areas. By choosing a local lender, you benefit from their insight and knowledge of the local market. Commitment to the Community Family Financial Services is more than just a lender; they are a dedicated member of the Corinth community. They actively participate in local events and support community initiatives, demonstrating their commitment to making a positive impact. When you choose Family Financial Services, you’re not just getting a loan; you’re supporting a business that cares about the well-being of your community. Conclusion Securing a loan doesn’t have to be a complicated or stressful process. Family Financial Services in Corinth, Mississippi, simplifies the loan process with their user-friendly application options, fast approval and funding, competitive rates, personalized customer service, and local expertise. Whether you need a personal loan, cash loan, or payday loan, Family Financial Services is dedicated to providing the financial support you need with the simplicity and care you deserve. Contact Family Financial Services today to learn more about their loan products and how they can help you achieve your financial goals.

The body content of your post goes here. To edit this text, click on it and delete this default text and start typing your own or paste your own from a different source.

For entrepreneurs and small business owners in Corinth, Mississippi, securing a business loan can be a pivotal step in expanding operations, managing cash flow, or investing in new opportunities. Family Financial Services offers a range of business loan options designed to support local businesses. In this guide, we will explore the various business loan opportunities available in Corinth, MS, and provide insights on how to navigate the application process successfully. Types of Business Loans 1. Term Loans Overview Term loans are a common type of business loan that provides a lump sum of money, repaid over a fixed period with a set interest rate. These loans are suitable for a variety of business needs, such as purchasing equipment, expanding operations, or refinancing existing debt. Benefits Fixed Repayment Schedule: Predictable monthly payments make budgeting easier. Flexible Use of Funds: Can be used for various business purposes. Competitive Interest Rates: Often lower than other types of financing. 2. Lines of Credit Overview A business line of credit provides access to a pool of funds that you can draw from as needed. You only pay interest on the amount you use, making it a flexible financing option for managing cash flow and covering unexpected expenses. Benefits Flexibility: Use funds as needed and only pay interest on the amount borrowed. Revolving Credit: Funds become available again once repaid. Short-Term Financing: Ideal for managing cash flow gaps and short-term needs. 3. Equipment Financing Overview Equipment financing allows businesses to purchase or lease equipment by using the equipment itself as collateral. This type of loan is specifically designed for acquiring machinery, vehicles, or other essential business equipment. Benefits Preserve Cash Flow: Spread the cost of expensive equipment over time. Collateralized Loan: Lower interest rates due to the collateral. Immediate Access to Equipment: Acquire necessary equipment without large upfront costs. 4. SBA Loans Overview Small Business Administration (SBA) loans are government-backed loans that provide favorable terms and lower interest rates. SBA loans are designed to support small businesses and come with various programs tailored to different needs. Benefits Favorable Terms: Lower interest rates and longer repayment periods. Government-Backed: Reduced risk for lenders, increasing approval chances. Versatile Programs: Various loan programs to meet different business needs. 5. Merchant Cash Advances Overview A merchant cash advance provides a lump sum of money in exchange for a percentage of future credit card sales. This type of financing is suitable for businesses with steady credit card sales looking for quick access to funds. Benefits Quick Access to Funds: Fast approval and funding process. Flexible Repayment: Repayments are based on a percentage of daily sales. No Collateral Required: Approval based on sales volume rather than credit score. How to Apply for a Business Loan in Corinth, MS 1. Assess Your Financial Needs Before applying for a business loan, determine how much funding you need and what you plan to use it for. Create a detailed business plan that outlines your goals, how the loan will help you achieve them, and how you plan to repay the loan. 2. Check Your Credit Score Both personal and business credit scores can impact your loan approval and interest rates. Check your credit scores and review your credit reports for any errors. Addressing any issues beforehand can improve your chances of securing favorable loan terms. 3. Gather Necessary Documentation Lenders will require various documents to assess your loan application. Commonly required documents include: Business Plan: Detailed plan outlining your business goals and loan purpose. Financial Statements: Income statements, balance sheets, and cash flow statements. Tax Returns: Personal and business tax returns for the past few years. Legal Documents: Business licenses, incorporation documents, and ownership agreements. 4. Research Lenders Explore different lenders to find the best loan options for your business. Family Financial Services in Corinth, MS, offers competitive rates and personalized service to help you find the right loan. Compare their terms with other local and online lenders to ensure you get the best deal. 5. Submit Your Application Once you have gathered all the necessary documentation, submit your loan application. Ensure all information is accurate and complete to avoid delays. Family Financial Services offers both online and in-person application options for your convenience. 6. Review Loan Offers After submitting your application, review the loan offers you receive. Pay attention to the interest rate, repayment terms, fees, and any other conditions. Choose the offer that best aligns with your business needs and financial situation. 7. Accept the Loan and Receive Funds Once you have selected the best loan offer, sign the loan agreement to accept the terms. The lender will then disburse the funds to your business account, typically within a few days. Tips for Successfully Securing a Business Loan Build a Strong Business Plan A well-crafted business plan is crucial for securing a loan. It demonstrates your understanding of the market, your business strategy, and how you plan to use the loan to achieve your goals. Be clear and concise, highlighting your business's strengths and potential for growth. Maintain Good Financial Records Accurate and up-to-date financial records are essential for loan approval. Keep detailed records of your income, expenses, and financial projections. This will help you present a clear picture of your business's financial health to lenders. Improve Your Credit Score Improving your personal and business credit scores can increase your chances of securing favorable loan terms. Pay down existing debts, make timely payments, and correct any errors on your credit reports. Shop Around Don't settle for the first loan offer you receive. Compare different lenders and loan options to find the best terms for your business. Consider both local lenders like Family Financial Services and online lenders to ensure you're getting the best deal. Be Prepared to Provide Collateral Some business loans may require collateral, such as equipment, inventory, or real estate. Be prepared to offer collateral if needed, and understand the risks involved. Conclusion Securing a business loan in Corinth, Mississippi, can provide the financial support you need to grow and expand your business. By understanding the different types of business loans available and following the steps outlined in this guide, you can navigate the application process successfully. Family Financial Services offers a range of business loan options and personalized support to help you achieve your business goals. Whether you need a term loan, line of credit, equipment financing, SBA loan, or merchant cash advance, they are here to provide the financial solutions you need to succeed.

Credit scores play a pivotal role in the lending process, influencing your ability to secure a loan and the terms you'll be offered. For residents of Corinth, Mississippi, understanding how credit scores impact loan approval can help you navigate the borrowing process more effectively. In this guide, we'll explore the importance of credit scores, how they affect loan eligibility and interest rates, and tips for improving your credit score. What is a Credit Score? Definition and Components A credit score is a numerical representation of your creditworthiness, based on your credit history. It ranges from 300 to 850, with higher scores indicating better credit health. Credit scores are calculated using several factors, including: Payment History: Your record of on-time payments is the most significant factor, accounting for about 35% of your score. Credit Utilization: This refers to the amount of available credit you're using, comprising about 30% of your score. Length of Credit History: The age of your credit accounts makes up around 15% of your score. Types of Credit: A mix of different credit types (e.g., credit cards, installment loans) accounts for about 10% of your score. Recent Credit Inquiries: New credit inquiries and accounts make up the remaining 10% of your score. Importance of Credit Scores in Loan Applications Loan Eligibility Lenders use credit scores to assess the risk of lending money to borrowers. A higher credit score indicates a lower risk of default, making you more likely to be approved for a loan. Conversely, a lower credit score can signal a higher risk, potentially leading to loan denial or the need for a co-signer. Interest Rates Credit scores also influence the interest rates you're offered. Borrowers with higher credit scores typically qualify for lower interest rates, reducing the overall cost of the loan. Lower credit scores can result in higher interest rates, increasing the amount you'll pay over the life of the loan. Loan Terms In addition to eligibility and interest rates, your credit score can affect other loan terms, such as the repayment period and loan amount. Lenders may offer more favorable terms to borrowers with strong credit profiles, providing greater flexibility and affordability. Impact of Credit Scores on Different Types of Loans Personal Loans For personal loans, lenders heavily weigh your credit score when determining approval and interest rates. A high credit score can help you secure a larger loan amount with a lower interest rate, making it easier to manage your monthly payments. Auto Loans Credit scores are crucial for auto loans, influencing both approval and the interest rate. Borrowers with excellent credit can often negotiate better loan terms, while those with lower scores may face higher rates or the need for a larger down payment. Cash Loans and Payday Loans While cash loans and payday loans are typically easier to obtain than traditional loans, credit scores can still play a role. Some lenders may use your credit score to determine the loan amount and terms, with higher scores potentially leading to better offers. How to Check Your Credit Score Free Credit Reports You can obtain a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year through AnnualCreditReport.com. Reviewing your credit report can help you identify any errors or discrepancies that may be affecting your score. Credit Monitoring Services Consider using credit monitoring services to keep track of your credit score and receive alerts about any changes. These services can help you stay informed and take proactive steps to maintain or improve your credit health. Tips for Improving Your Credit Score Pay Your Bills on Time Consistently making on-time payments is the most effective way to improve your credit score. Set up automatic payments or reminders to ensure you never miss a due date. Reduce Credit Card Balances Lowering your credit card balances can improve your credit utilization ratio, positively impacting your score. Aim to keep your utilization below 30% of your available credit. Avoid Opening Too Many New Accounts Opening multiple new credit accounts in a short period can negatively affect your credit score. Apply for new credit only when necessary and focus on maintaining your existing accounts. Dispute Errors on Your Credit Report Review your credit report for any inaccuracies, such as incorrect account information or fraudulent activity. Dispute any errors with the credit bureau to have them corrected and improve your score. Diversify Your Credit Mix Having a mix of credit types, such as credit cards, installment loans, and mortgages, can enhance your credit profile. However, only take on new credit if it fits within your financial plan and you can manage it responsibly. Keep Old Accounts Open The length of your credit history contributes to your credit score, so keep older accounts open, even if you no longer use them frequently. Closing old accounts can shorten your credit history and lower your score. Conclusion Your credit score is a crucial factor in securing loans in Corinth, MS, affecting your eligibility, interest rates, and loan terms. By understanding the importance of credit scores and taking steps to improve and maintain your score, you can enhance your borrowing prospects and secure more favorable loan conditions. Family Financial Services is committed to helping you navigate the loan process and achieve your financial goals. Whether you need a personal loan, auto loan, or cash loan, their team is here to provide the support and guidance you need to make informed financial decisions.

Applying for a loan can be a crucial step in achieving your financial goals, whether it’s for managing unexpected expenses, consolidating debt, or making a major purchase. However, the process can be fraught with potential pitfalls. To help you navigate the application process successfully, here are five common mistakes to avoid when applying for a loan in Corinth, Mississippi. 1. Not Checking Your Credit Score Importance of Credit Score Your credit score plays a significant role in determining your eligibility for a loan and the interest rate you'll be offered. Lenders use your credit score to assess your creditworthiness and the risk associated with lending you money. A higher credit score generally means better loan terms and lower interest rates. Common Mistake One of the most common mistakes borrowers make is not checking their credit score before applying for a loan. Without knowing your credit score, you could be blindsided by a loan rejection or an unexpectedly high interest rate. How to Avoid Before applying for a loan, check your credit score and review your credit report for any errors or discrepancies. You can obtain a free credit report from each of the three major credit bureaus once a year through AnnualCreditReport.com. If you find any inaccuracies, dispute them promptly to improve your score. 2. Borrowing More Than You Need Assessing Your Financial Needs It can be tempting to borrow more money than you actually need, especially if you qualify for a larger loan amount. However, borrowing more than necessary can lead to higher monthly payments and increased interest costs over the life of the loan. Common Mistake Many first-time borrowers make the mistake of borrowing the maximum amount they qualify for, rather than the amount they actually need. This can strain your finances and make it harder to meet your repayment obligations. How to Avoid Carefully assess your financial needs and determine the exact amount you require before applying for a loan. Create a detailed budget that outlines your income, expenses, and the specific amount you need to borrow. Stick to this amount to avoid unnecessary debt. 3. Not Comparing Loan Options Exploring Different Lenders Not all loans are created equal. Different lenders offer varying interest rates, fees, and terms. Failing to compare loan options can result in higher costs and less favorable terms. Common Mistake Many borrowers make the mistake of accepting the first loan offer they receive without shopping around. This can lead to missing out on better deals and more favorable loan terms. How to Avoid Take the time to compare loan offers from multiple lenders. Look at interest rates, repayment terms, fees, and customer reviews. Use online comparison tools to make the process easier. By comparing different options, you can find the best loan for your needs and save money in the long run. 4. Ignoring the Fine Print Understanding Loan Terms The terms and conditions of a loan agreement can significantly impact your financial well-being. Ignoring the fine print can lead to unexpected costs, penalties, and repayment challenges. Common Mistake A common mistake is not reading the loan agreement thoroughly before signing. Borrowers may overlook important details such as interest rates, repayment terms, fees, and penalties for late payments or early repayment. How to Avoid Carefully read and understand the terms and conditions of the loan agreement before signing. Pay attention to the interest rate, repayment schedule, fees, and any penalties. If there are any terms you don’t understand, ask the lender for clarification. Ensuring you fully understand the agreement can prevent surprises and help you manage your loan effectively. 5. Failing to Create a Repayment Plan Importance of Repayment Planning A well-thought-out repayment plan is essential for managing your loan and avoiding default. Without a plan, you may struggle to make timely payments, which can negatively impact your credit score and financial health. Common Mistake Many borrowers fail to create a detailed repayment plan before taking out a loan. This can lead to missed payments, late fees, and increased interest costs. How to Avoid Before accepting a loan, create a comprehensive repayment plan that outlines how you will make your monthly payments. Consider your income, expenses, and any other financial obligations. Ensure you have enough income to cover the loan payments without sacrificing other essential expenses. Setting up automatic payments can also help you stay on track and avoid late fees. Conclusion Avoiding these common mistakes can help you navigate the loan application process successfully and secure the best loan for your needs. By checking your credit score, borrowing only what you need, comparing loan options, understanding the fine print, and creating a repayment plan, you can make informed decisions and achieve your financial goals. Family Financial Services in Corinth, Mississippi, is here to provide the support and guidance you need throughout the loan application process. By partnering with a trusted local lender, you can confidently secure the financial resources you need and manage your loan effectively.

When it comes to securing a loan, finding the right lender is just as important as choosing the right type of loan. For residents of Corinth, Mississippi, Family Financial Services stands out as a trusted and reliable provider of financial solutions. In this blog, we'll explore the top reasons why Family Financial Services is the best choice for your loan needs in Corinth, MS. 1. Local Expertise and Personalized Service Understanding the Community Family Financial Services is deeply rooted in the Corinth community. As a local lender, they understand the unique financial needs and challenges faced by residents. This local expertise allows them to offer personalized loan solutions that cater specifically to the community's requirements. Personalized Attention Unlike large, impersonal banks, Family Financial Services takes the time to get to know their clients. They offer personalized service, taking into account your individual financial situation and goals. This tailored approach ensures that you receive the best loan option for your needs, with terms that are manageable and beneficial. 2. Wide Range of Loan Options Versatility in Lending Family Financial Services offers a comprehensive range of loan products, including: Cash Loans Personal Loans Same-Day Loans Payday Loans This versatility means that no matter your financial situation or need, there's a loan option available for you. Quick Loans for Immediate Needs For those unexpected expenses or urgent financial needs, Family Financial Services provides quick loan options such as same-day loans and payday loans. These loans are designed to offer fast access to funds, ensuring you can address emergencies without delay. 3. Competitive Interest Rates and Terms Affordable Financing One of the key benefits of choosing Family Financial Services is their competitive interest rates. They strive to offer affordable financing options that help you save money over the life of your loan. By providing reasonable rates and favorable terms, they make it easier for you to manage your repayments and achieve your financial goals. Flexible Repayment Plans Family Financial Services understands that everyone's financial situation is different. That's why they offer flexible repayment plans that can be tailored to fit your budget. Whether you need a shorter-term loan with higher monthly payments or a longer-term loan with lower payments, they work with you to find the best solution. 4. Simplified Application Process Easy and Convenient Applying for a loan with Family Financial Services is straightforward and hassle-free. They offer both online and in-person application options, allowing you to choose the method that's most convenient for you. The application process is designed to be quick and easy, with minimal paperwork required. Fast Approval and Funding When you need a loan, time is often of the essence. Family Financial Services prides itself on fast approval times, often providing decisions within hours. Once approved, funds are typically disbursed quickly, ensuring you have access to the money you need without unnecessary delays. 5. Commitment to Customer Satisfaction Exceptional Customer Service At Family Financial Services, customer satisfaction is a top priority. Their friendly and knowledgeable staff are always ready to assist you with any questions or concerns you may have. They take the time to explain loan terms and conditions, ensuring you fully understand your agreement before signing. Ongoing Support Family Financial Services is committed to supporting their clients throughout the life of their loans. If you encounter any issues or have difficulty making payments, their team is available to work with you to find a solution. This ongoing support helps you manage your loan effectively and maintain your financial health. 6. Community Involvement Giving Back As a local business, Family Financial Services is dedicated to giving back to the Corinth community. They actively participate in local events, support charitable organizations, and contribute to community development projects. By choosing Family Financial Services, you’re not just getting a loan; you’re also supporting a company that cares about the well-being of your community. Building Relationships Family Financial Services values long-term relationships with their clients. They aim to be more than just a lender; they strive to be a trusted financial partner. By providing reliable service and building strong relationships, they have earned the trust and loyalty of many Corinth residents. Conclusion Choosing the right lender is a critical step in securing a loan that meets your needs and helps you achieve your financial goals. Family Financial Services in Corinth, MS, offers numerous advantages, including local expertise, personalized service, a wide range of loan options, competitive rates, a simplified application process, and a commitment to customer satisfaction. Their dedication to the community and focus on building long-term relationships make them the ideal choice for your loan needs. Whether you need a cash loan, personal loan, same-day loan, or payday loan, Family Financial Services is here to provide the financial support you need with the personalized attention you deserve.

Securing a loan for the first time can be a daunting task, but understanding the available options and knowing what to expect can make the process much smoother. If you're a first-time borrower in Corinth, Mississippi, Family Financial Services offers a variety of loan options tailored to meet your financial needs. In this guide, we will explore the best loan options for first-time borrowers, including cash loans, personal loans, same-day loans, and payday loans. 1. Cash Loans What are Cash Loans? Cash loans are short-term loans that provide borrowers with a lump sum of money, typically repaid over a short period, such as a few weeks or months. These loans are ideal for covering unexpected expenses or emergencies. Benefits of Cash Loans Quick Access to Funds: Cash loans offer fast approval and funding, often within the same day. Flexible Use: You can use the funds for various purposes, such as medical bills, car repairs, or home emergencies. Simple Application Process: The application process is straightforward, with minimal documentation required. How to Apply for a Cash Loan To apply for a cash loan at Family Financial Services in Corinth, MS, you will need to provide basic information, such as proof of income, identification, and your bank account details. The application can be completed online or in-person for your convenience. 2. Personal Loans What are Personal Loans? Personal loans are unsecured loans that provide borrowers with a lump sum of money, repaid in fixed monthly installments over a set period. These loans are versatile and can be used for various financial needs. Benefits of Personal Loans Fixed Interest Rates: Personal loans typically come with fixed interest rates, providing predictable monthly payments. Flexible Repayment Terms: Repayment terms can range from a few months to several years, allowing you to choose a term that fits your budget. Versatility: Personal loans can be used for debt consolidation, home improvements, education expenses, and more. How to Apply for a Personal Loan To apply for a personal loan, gather the necessary documentation, such as proof of income, identification, and details about your financial situation. Submit your application online or visit Family Financial Services in Corinth, MS, for personalized assistance. 3. Same-Day Loans What are Same-Day Loans? Same-day loans are short-term loans designed to provide quick access to funds, typically within the same day of application. These loans are ideal for urgent financial needs. Benefits of Same-Day Loans Immediate Funding: Same-day loans offer fast approval and funding, often within hours of application. Easy Application: The application process is simple, with minimal paperwork required. Emergency Use: These loans are perfect for covering urgent expenses, such as medical emergencies or unexpected car repairs. How to Apply for a Same-Day Loan To apply for a same-day loan at Family Financial Services in Corinth, MS, you will need to provide proof of income, identification, and your bank account details. The application can be completed quickly online or in-person. 4. Payday Loans What are Payday Loans? Payday loans are short-term, high-interest loans designed to provide immediate cash that is repaid on your next payday. These loans are suitable for small, urgent financial needs. Benefits of Payday Loans Fast Approval: Payday loans offer quick approval and funding, often within the same day. No Credit Check: These loans typically do not require a credit check, making them accessible to borrowers with poor credit. Convenient Repayment: Repayment is due on your next payday, making it easy to manage. How to Apply for a Payday Loan To apply for a payday loan, you will need to provide proof of income, identification, and your bank account details. Family Financial Services in Corinth, MS, offers a streamlined application process to get you the funds you need quickly. Tips for First-Time Borrowers Understand Your Financial Needs Before applying for a loan, assess your financial needs and determine how much money you require. This will help you choose the right loan option and avoid borrowing more than necessary. Check Your Credit Score Your credit score plays a significant role in determining your eligibility for certain loans and the interest rate you'll receive. Check your credit score and review your credit report for any errors or discrepancies. If your credit score is lower than expected, take steps to improve it before applying for a loan. Compare Loan Options Take the time to compare different loan options and lenders. Consider factors such as interest rates, repayment terms, fees, and eligibility requirements. Family Financial Services in Corinth, MS, offers competitive rates and personalized service to help you find the best loan option for your needs. Read the Fine Print Before accepting a loan, carefully read the terms and conditions. Pay attention to the interest rate, repayment schedule, fees, and any penalties for late payments. Make sure you understand all aspects of the loan agreement to avoid any surprises. Create a Repayment Plan Once you secure a loan, create a detailed repayment plan that outlines how you'll make your monthly payments. Factor the loan payment into your budget and ensure you have enough income to cover it without sacrificing other essential expenses. Communicate with Your Lender If you encounter any issues with repaying your loan, don't hesitate to communicate with your lender. Family Financial Services is committed to helping borrowers succeed and may offer solutions such as payment extensions or modified repayment plans. Open communication can prevent misunderstandings and help you manage your loan effectively. Conclusion Securing a loan for the first time in Corinth, Mississippi, doesn't have to be a stressful experience. By understanding the different loan options available, such as cash loans, personal loans, same-day loans, and payday loans, you can make an informed decision that meets your financial needs. Family Financial Services offers a range of loan products and personalized support to guide you through the process. By following the tips outlined in this guide, you can confidently navigate the loan application process and achieve your financial goals.